Interaction between the Insurance Industry and the Local Economy

Rose Neng LAI*

Abstract

Being a major participant in the financial sector, the insurance industry has played a non-trivial role in the prosperity of the economy of Macau. In turn,the uniqueness and characteristics of the structure and policies of the local economy have helped build up attractions for more international insurance companies to set up their branches in Macau. This paper serves to provide a preliminary discussion on the mutual influences as well as the future prospectsof the local insurance market.

1.Introduction

From the financial point of view, any idle money should be deposited into bank savings accounts because of time value of money. Besides depositing inbanks and earning the interest virtually free from risk, people may be more attracted to investments with high return, albeit higher risk. This is why the financial markets in the world can be so active.

In fact, financial markets constitute the biggest markets in the world. People who are more risk averse, that is, reluctant to be exposed to risk, will be more inclined to invest in investment trusts, which are pools of money managed and invested by financial intermediaries on behalf of their clients. Other forms of less risky investments are government bonds.

Traditionally, when Chinese people retired, their sons and daughters wouldbe responsible of supporting them. Now that this Chinese culture has changed,there has been a substantial increase in the need for funds to achieve the goal of providing income benefits after retirement. Given this, it would be crucial to establish personal investments for such purpose. When the goal of investment is solely to safely accumulate wealth for the future, risky assets will definitely not be a choice. Rather, people will choose either provident funds or pension funds. The objective of such funds is to pile up resources to be used to provide income benefits after retirement. Although these are also pools of money managed by financial institutions, the investments encountered will be much less risky. One group of participants in managing such funds is the insurance industry.

This paper serves to discuss the role of the local insurance companies inmanaging investment funds. The next section presents how insurance policies can act as a mean of investment tools. Section 3 reviews the insurance industry in Macau; while Section 4 introduces a relatively new profession in the industry that enhances the investment function of insurance. Section 5 discusses themeasures for quality assurance of the industry. Finally, Section 6 concludes.

2.Insurance as Investment Tools

2.1 The Need for the Insurance Industry

Chinese are well known for heavy savings. Due to the unpleasant history of the past century, most Chinese people have been trained to save most of what they earn. Such tradition can be reflected by the common Chinese saying,"reserve crops to prevent starvation".Compared to the Western counterparts,Chinese families tend to have very modest expenditure.

As China has begun its open door policy since the early 1980s,this culture has changed remarkably over the past two decades. Retail markets have experienced extensive expansion both in quantity/quality and in variety. People are more eager to spend for leisure over basic necessities. Nevertheless, the long tied tradition is still apparent. Savings still constitute a significant proportion of household income. However, the tools enhancing such purpose have been developed from the very traditional uninteresting savings in bank accounts to avariety of channels. For instance, people in China are very keen on investing in local stock markets. More investment tools have been welcomed to the economy.

In Macau, household savings are also remarkable. The average grossdomestic savings rate, which is the domestic savings as a percentage of gross domestic products, was around 53% for the period 1983-2000. This iscomparatively high by international standards.1 Investments methods in Macauon the other hand are very limited. Besides establishing individual smallbusinesses, typical drains of savings are mostly confined to savings accountsand fixed deposits in banks.

With the lack of any financial markets such as stock and futures exchanges or bond markets, tools in the form of investments in company shares are available only from local banks and a few financial firms, which are branches of financial firms in Hong Kong. Banks also provide a limited variety of investment trusts.However, these trusts funds are products of financial intermediaries in HongKong. In other words, the portfolios are not catered to the needs and riskpreferences to locals.

Roughly speaking, life assurance policies are the only types of investments in Macau that are tailored individually according to the income levels and investment preferences of the clients. Certainly, another form of investments that depends mainly on income level is pension fund or provident fund. However,as Macau lacks a mandatory provident fund scheme like that of its vicinity,Hong Kong, the provision of such funds solely depends on the discretion of organizations. Nor does it have any compulsory pension funds scheme other than those for civil servants and the social security funds. In Macau, pension fund schemes are not widely applied. According to The Monetary Authority of Macau, only 4% of the over 200 hundred thousand working population has joined some private pension funds. Thus, when people retire, the only periodical funds that they are entitled to would be limited to the monthly social security funds(which amounts to MOP1,000 per month as of the current year), provided that they made their contribution while at work (which amounts to MOP15.00per month). Thus, life insurance policies make up the most common form ofinvestment after bank savings for the Macau citizens.

2.2 Brief Review of Insurance Policies

Insurance is normally classified into four categories, namely the property-liability insurance, life insurance, health insurance and retirement programs.Of these categories, only the second and the last are aimed for investment purpose. All others are purely insured against risk; and no savings component is present. When a whole life insurance policy incorporates an investment element, the holder of the policy will have to pay extra amount for investment purposes on top of the cost of life insurance providing the same death benefit.On the other hand, this investment element results in additional benefits that donot require the insured's death to become available.

Insurance for investment purposes can again be subdivided into savings insurance and investment insurance. Savings insurance incorporates both pure life insurance and dividend yields, and is the most widely accepted type of insurance. Some of these plans come in the form of term insurance, which provides insurance for a specified time period. Investment insurance allows policyholders to select their own investment portfolios for excess returns in addition to pure life insurance.Many insurance companies will launch different investment plans to the customers to cater their different investment purposes.For instance, there are plans for children's education, different kinds ofinvestment-linked life insurance that provide different possible rates of returnsubject to variable levels of risks and retirement savings plans.

In general, a life insurance policy constitutes benefit provision and financing provision. The former is the ultimate feature incorporated in all insurances, that is, what the insurer promises to pay under certain circumstances specified in the policy. The latter provision specifies the payment schemes such as (1) single-premium insurance, whereby the premium is paid only once in a lump sum, (2)straight life insurance, which is financed with installment premiums for as long as the life of the insured, and (3) limited-pay insurance, with which the insured pays installment premiums until the age specified in the policy (for example,paid-up at age 65). In fact, annually renewable term insurance can also be viewed as a life insurance if it can be renewed for life. Nevertheless, most of these policies have a limited right of renewal of, for example, up to age 70.2 From these payment schemes, it is easy to see that a person with constant inflow of funds available for investment can hold an insurance policy constituting investment elements by paying the annual premium until retirement. Normally,the insured amount of a typical life policy should amount to 10 to 15 years of annual income, which requires an annual premium of roughly 10% of annualincome.

2.3 Life Insurance Market in Hong Kong --A Comparison

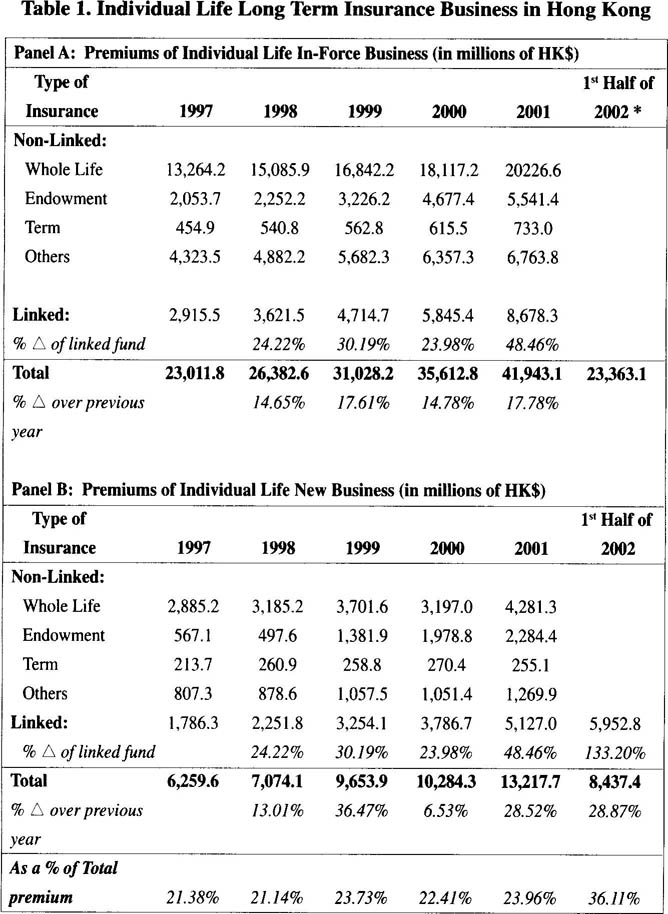

The insurance industry in Hong Kong is still experiencing fast growth,despite being already well established. The total life insurance premium received from new life policies in the first two quarters of 2002 in Hong Kong amounts to HK$8.4billion (see Table 1). The average annual premium per policyholder is HK$20,110.55. The total premiums from all types of insurance contribute to 5.9% of the Gross Domestic Product of Hong Kong. Despite this, there is still ahuge potential in the business. A Hong Kong newspaper once sited that themarket penetration rate of 70%, compared with over 100% of the U.S. and almost 400% of Japan, is relatively low..3

According to the statistics from the Office of the Commissioner of Insurance of Hong Kong, there are altogether 199 authorized insurance companies in Hong Kong as at the end of September 2002, of which 132 are pure general insurers,48 are pure long-term (mostly life insurance) insurers and 19 composite insurers.In terms of participants, as the end of the same date, there are 423 authorized insurance brokers, 3,321 chief executives/technical representatives of the authorized brokers, 2,053 insurance agencies, 29,963 individual agents, 2,053responsible officers and 14,946 technical representatives registered with theInsurance Agents Registration Board (IARB).

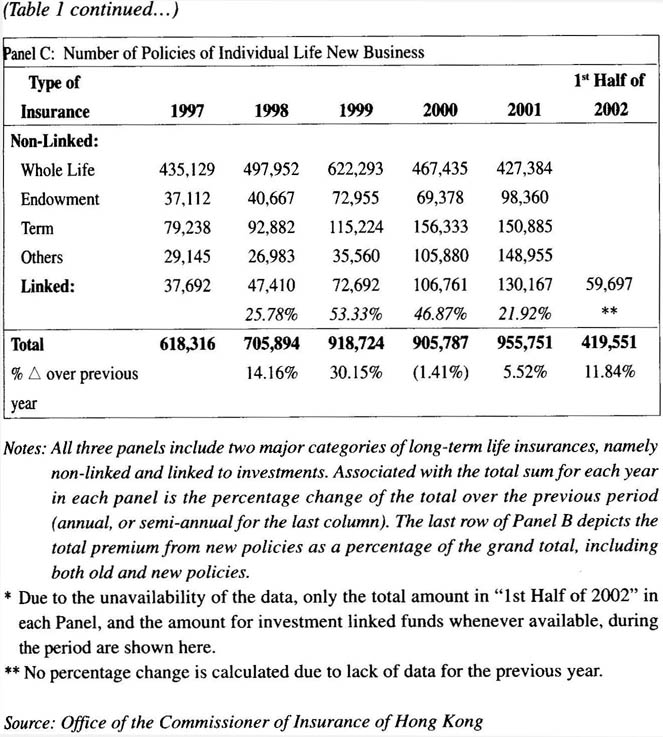

As far as life insurance is concerned, Table 1 depicts the total premiums, premiums from new business, and the number of new contracts for life insurance for the last five years as well as the first half of year 2002. From the percentage change of the total linked life premium in Panel A of the Table, it is apparent that the investment-linked life insurance is gaining more momentum to become a major component next to whole life insurance in life insurance. This reflects that more people are increasingly concerned about earning stable and generous return from the insurance premium in addition to pure insurance and savings,so as to ensure more funding availability after retirement. More evidence can be observed from Panel C of the Table, in which there are always substantial increases in the number of policies year after year. This also implies that investment linked policies have attracted a broad clientele. To see this, notice that the new premiums in Panel B increase by smaller percentages than the number of new contracts in 1998-2000. This shows that more people with fewer earnings have joined the market, resulted in smaller average premium percontract. Another observation is that the amount of whole life insurance, which is essentially savings insurance, mostly increases steadily over the period of study, which again confirms the importance of savings via insurance.

A further interesting finding is that insurance has apparently become a shelter during economic downturn. To see this, notice that the period of study in Table 1 includes the Asian Crisis that occurred at the end of 1997, which is followed by the gloomy economy in Hong Kong over the years concerned.Contradicting the economic trend, new life insurance policies, especially those linked to investments, have maintained their importance. In sum, there is still plenty of rooms for the insurance industry to grow in Hong Kong.

3. The Local Insurance Industry

There are currently 9 life assurance companies and 15 non-life insurancecompanies in Macau as at the end of 2001.In the same period,the total numberof employees of the licensed companies totaled to 332,while there are a total of 1,991(42.1% increased from 2001) individual agents,46 corporate agents(upby 1 from 37 local corporate agents and 8 overseas corporate agents in the previous year), 15 salesmen (down from 16 last year) and 7 overseas brokers.4 All licensed insurance companies or insurance intermediaries are authorized to carry out insurance business and/or reinsurance of any insurance contracts.

The local insurance businesses can be broadly classified into two categories. The first is the compulsory insurance, which is subdivided into motor vehicle (third party risks) insurance, employees' compensation insurance, professional liability insurance for travel agents, public liability insurance relating to the fixing of propaganda and publicity materials, and the third party liability for pleasure boats. The second type is the voluntary insurance, which includes private pension funds, and is essentially the life assurance that can be considered as personal investments. Another way of classifying insurance identical to that of Hong Kong is life insurance versusnon-life insurance. Life insurances include life and annuity, marriage and birth, linked long term, health, long term, short term, tontines, capital redemption, pension fund management Type 1, 2 and 3, and operations of capitalization. Non-life insurances are composed of accident (personal and occupational), sickness, land vehicles, railway rolling stock, aircraft, ships,goods in transit, fire and natural forces, damage to property, motor vehicle liability, aircraft liability, liability for ships, general liability, credit(commercial risks), suretyship, miscellaneous insurance on financial loss,and legal expenses.5 This classification reveals the completeness of the Macau insurance industry, although some of them might have never been written.

Table 2 depicts the gross premiums situation in the insurance industry of Macau for the period of 1999 to June 30th, 2002. The gross premiums for the first quarter of 2002 amounted to a total of MOP339.83 million, of which MOP218.76 million was from life insurance and MOP121.069 million was from non-life insurance. This represents an increase of respectively 28.1% and 11.2% from the same quarter of the previous year.6A comparison from the last two columns of Table 2 reveals a total lifeinsurance premium of MOP237.01 million in the second quarter of 2002,which denotes an 8.34% increase from the first quarter. In addition, thetotal gross premium constitutes 2.59% of the expenditure-based grossdomestic product (GDP) in 2001.7

Table 2. Gross Premiums of Insurance in Macau(in million MOP)

┌─────────────────────────────────────────┐

│Type of 1st Quarter of 1st Half of│

│Insurance 1999 2000 2001 2002 2002 │

├─────────────────────────────────────────┤

│Life 667.056 755.327 928.854 218.763 455.774 │

│ 27.8% 13.2% 23.0% 28.1% 18.2% │

│Non-Life 365.620 347.920 358.956 121.069** 490.645* │

│ (7.9%) (4.8%) 3.2% 11.2% 162.2% │

│Total 1,032.676 1,103.247 1,287.810 339.832 946.428 │

│ (12.4%) 6.8% 16.7% 21.5% 65.3% │

├─────────────────────────────────────────┤

│Life as % of 64.59% 68.46% 72.13% 64.37% 48.16% │

│Total 69.11%# │

└─────────────────────────────────────────┘

|

Notes: Associated with each amount is the percentage change compared with the previous period (annual, quarterly, or semi-annual). The last row of the Table depicts the total premium from life policies as a percentage of the grand total, including both life and non-life policies.

*Note that the non-life premium for 1st half of 2002 has soared significantly due to the MOP286.912 (or 11,548.9% from the same period of the previous year) remarkable increase in reinsurance of miscellaneous non-life accident. Ignoring this category reflects a non-life insurance amount of only MOP203.733.

**It is suspected that the noticeable 11.2% increase in non-life insurance premium is also due to abnormal increase in the reinsurance category, although the lack of information prohibits further verification.

#If the reinsurance premium mentioned in note * is deducted, the total life premium for the first half of 2002 amounts to 69.11% of the total premium.

Source: AMCM 2001 Annual Report, AMCM 2002 Macau Insurance Activity Quarterly Report, and AMCM 2002 Macau Insurance Activity Semi-annual Report.

The last row of Table 2 also shows that life insurance has consistently contributed over two-thirds of gross insurance premiums. For instance, gross premiums from life insurance for the year of 2001 represents a market share of 72.1%, which is also a 23% increase from the previous year. Note that the non-life premium for 1st half of 2002 has soared significantly due to the MOP286.912(or 11,548.9% from the same period of the previous year) remarkable increase in reinsurance of miscellaneous non-life accident. Ignoring this category reflectsa total life premium for the first half of 2002 of 69.11% of the total premium. In fact, it is suspected that the noticeable 11.2% increase in non-life insurance premium is also due to abnormal increase in the reinsurance category, although lack of information prohibits further verification. Thus, the life insurance premiums in general increase consistently over the period.

Given the continual dominance of life insurance in the insurance industry,the issue is hence whether there exists any expansion potential, and to what extent. To see this, comparisons from several aspects between the two neighboring cities, that is, Hong Kong and Macau, are performed. Firstly, the gross life premium of MOP455.77 million in the first half of 2002 in Macau is only about1.95% of HK$23,363.1 million in Hong Kong (note that HK$1.00=MOP1.032), although the population is around 7% of that of Hong Kong(crowded in less than 2.5% of the land in Hong Kong). This apparently implies either that fewer Macau people hold life insurance policies, or that the policies are not written with high premiums.

In fact, participants of the local industry reveal that, except for those earning the top 5% of monthly income in Macau (which constitutes only a small population proportion), the average annual premium per life insurance policy is only around MOP5,000.00, which is only one-quarter of that in Hong Kong (as seen from Table 1).8 Would the small premium be possibly due to the lower personal income? The data provided by the Census and Statistics Departments of both cities show that the median monthly earnings are MOP4,655.00 and HK$10,000.00 in 2001 for Macau and Hong Kong respectively. On the other hand, people in Hong Kong have to spend an average housing expenditure of over 50% of monthly income. Thus, even if all other expenditure are equally sizeable, the difference in annual premiums per policy should still be reasonably smaller. Since the already larger Hong Kong market still possesses rooms for expansion, there is little doubt that the insurance market in Macau has a huge room for growth. Recall that the gross life premiums of Macau is less than 2% of that of Hong Kong, while the insurance workforce is less than 7% of its counterpart, there should be enough manpower to support the growth momentum of the industry.

Furthermore, 1999 is still in the aftermath period from the Asian Crisis. In addition, the Macau economy has experienced years of negative growth. These may be the reasons why the amount of gross insurance premium decreased in 1999. Then, after the handover to China to become a Special Administrative Region, the territory has spun off from negative economic growth. This hasadded fuel to the increase in gross premium. Also obvious is the contribution of the insurance industry to the GDP of the economy as mentioned earlier. Thus, it is easy to see that a growing economy can help boost the insurance industry;while the growth in the industry in turn increases contribution to the economic growth. This"snowball rolling" effect reflects the importance and interactive mechanism between the industry and the economy. The current obstacle is perhaps to achieve a bigger market penetration, which can possibly be achieved more efficiently and effective through the profession of financial planning. This will be discussed in the next section.

4.The Role of Financial Planning in Insurance Companies

Traditionally, the concept of insurance has not been widely accepted by people in Macau, mostly because only a small proportion of insurance agents possess adequate knowledge in the area and be able to introduce the need and benefits to the potential customers. As a result,insurance agents, and hence insurance companies,are, commonly perceived as money collectors who do not provide much services and benefits in return. Over these years of government efforts to improve the economy and the standard of living in Macau, albeit negative economic growth in the late 1990s, people have gained more knowledge, and hence higher demand for life insurance as a mean of investment in addition to solely insurance purpose. Although the major services provided by insurance companies can be broadly classified into life assurance and non-life insurance, the wide range of personal income has motivated an increasing need of provision of newer and innovative products to cater to the need and desire of consumers.

Yet, this "tailor-making policy" service requires certain level of expertise in risk and insurance management. Therefore, the profession of financial planning that has earned wide recognition in well-developed economies such as the world-dominant United States has been introduced to the insurance industries in both gong Kong and Macau. The role of financial planners is to assist investors in formulating and implementing investment strategies that will meet with their long-term financial goals. Therefore, such profession is widely demanded by banking, insurance, investment management and securities industries that provide and distribute financial products to people with long term financial needs of the aging population.

To adhere to the rigorous quality of financial planners, the Certified Financial Planner (CFP) certification was introduced in 1972, and was regulated by the Certified Financial Planner Board of Standards, Inc., US (or CFP Board)which was founded in 1985. In Hong Kong, the regulatory body as well as the licensing authority of CFP was the Institute of Financial Planners of Hong Kong Limited (IFPHK) established in June 2000. Of course, not all the financial planners in the industries, at least neither in Hong Kong nor Macau, have been certified. Nevertheless, the increasing need for such profession has enticed more people to obtain the license of CFP.

To become a CFP, the candidate must possess knowledge of foundation of financial planning, investment, insurance, tax planning, retirement plans and employee benefits, and advanced financial planning. According to the IFPHK,he/she must be a university graduate with a minimum of three years full-time relevant working experience such as establishing client-planner relationship,gathering client data, determining goals and expectations, being able to analyze and evaluate client's financial status, developing, presenting, implementing and monitoring financial plans. If he/she does not have a recognized university degree, he/she must have a minimum of six years of full-time relevant working experience. He/she then has to pass the education, examination, experience and ethics requirements, as well as the continuing education requirements. He/she can then apply for the 10-hour Certification Examination. When all these requirements are satisfied, he/she will be granted the license. Under some special cases such as doctoral degree holders in business or economics or chartered financial analysts (CFA), the candidate can waive some of the requirements mentioned above. The passing rate of the Certification Examination since the establishment of IFPHK has never been high. In the second intake in June 2002,24% of the 1044 candidates (5.4 times that of the first intake) passed the examination. Subsequently, more than 200 candidates were granted the professional qualification (that is, already obtained relevant experiences), making up a total of 330 CFP in Hong Kong.9

In Macau, only the biggest insurance company, which comprises consistently over 50% of the market share, offers financial planning services.10Over the nine months ended on 31st August, 2002, its five new financial planners have successfully drawn a total first year premium of HK$724,878.00.11Although, overall statistics on the matter are unavailable, it is still easy to project the market potential of investment funds via personally fitted financial planning.Currently, none of these financial planners is a CFP. Therefore, the presentbenchmark for quality assurance is university education.Once employed,the financial planners will have to undergo some training programs to ensure their capability in providing clients with risk management,retirement,investment and savings planning.

5.How to Achieve Quality Assurance

Over the past decade, more people were willing to work as insurance agents,especially when the economy was at its downturn. It is because when manyindustries were affected in the economic bust, people from these industries wereuncertain about their future, and were therefore more willing to buy insurancepolicies. This caused a higher demand in insurance agents. Owing to the lessstringent entry barriers in those years, the qualifications of these insurance agentsbecame questionable. However, as the industry expands together with economicimprovement, it is utmost important to improve the overall quality of the industryparticipants. This section discusses the various measures that Macau has taken,and will take to ensure the quality of the insurance industry.

The supervisory body overlooking the local insurance market is theMonetary Authority of Macau (AMCM). The Insurance Supervision Departmentof the AMCM is responsible for supervising, coordinating and inspecting of allinsurance activities. Insurers have to abide by the "Macau Insurance CompaniesOrdinance" stated on Decree-Laws such as No. 27/97/M and No. 006/99/M,part of which are annexed with additional notices such as Notice No. 008/2000-AMCM and 009/2000-AMCM, and amended in 2001 as Law No. 10/2001. TheAMCM is constantly upgrading and improving services from the insuranceindustry through its supervision as well as enactment of new laws. For instance,it has issued the "Guidance Note on Prevention of Money Laundering inInsurance Business" in March 2001 with the aim of preventing any illegitimatefund making use of the insurance market in Macau for the stated purpose.

In terms of quality assurance of participants, the AMCM has introducedthe "Insurance Intermediaries Quality Assurance Scheme" to enhanceprofessional quality of the industry in order to protect the interests of the insuredpublic. This scheme has been implemented since January 1st, 2002. Under thescheme, all insurance intermediaries are required to pass the InsuranceIntermediaries Qualifying Examination unless exempt otherwise. Insuranceagents can be partially exempted, or fully exempted if they have transactedboth life and non-life insurance, from the examination if they have threeconsecutive years of experience in the industry prior to December 31 st, 2001 aswell as earning a first year commission of no less than MOP24,000.00.Otherwise, they will have to pass the examination within two years since January1 st, 2002, or from the day entering the industry. Those who wish to join theindustry after January 1 st, 2002 must be either secondary school graduates (thatis, completed form five education), or five years of relevant experience infinancial institutions, to be qualified to apply for the examination. As the currenttarget is to improve the qualification of insurance agents, there is no entryrequirement for financial planners yet. Nevertheless, as mentioned in the previoussection, the only insurance company that hires financial planners has its ownstandard of assurance. In time, qualification and requirements will surely becomemore rigorous as the market expands.

6.Conclusion

Two major causes prompting Macau residents with the essence ofinvestment are a lack of mandatory pension fund or provident fund scheme anda high savings rate. The former cause may lead to insufficient fund for spendingafter retirement. The latter results in suboptimal allocation of wealth, in which,if used properly should help boost up the overall economy. Given this, it will beessential to explore methods of investments. However, because investmentsnormally incur different levels of risks, it is crucial to choose an investment thatcan guarantee at least a modest return, and hence, a promising steady cashavailability after retirement. It is also necessary that the investment can be cateredfor personal needs. Insurance policies are good candidates of fulfilling suchgoals. Therefore, this paper discusses the role of insurance industry in facilitatinginvestment in Macau.

This paper covers the topic from different focuses. Firstly, the need forinsurance as well as the different classification of insurance are discussed. Then,since Hong Kong, being a close neighbor, is a good mirror of Macau in mostaspects, its insurance industry has to be introduced for comparison purpose.This is followed by the insurance market situations in Macau. From the twosections, it is obvious that the market in Macau is very small when compared tothat of Hong Kong. There are high potentials for both insurance markets togrow, and even more so for that of Macau because its residents apparently havenot devoted enough funds for their insurance policies, especially those long-term life policies or those linked to investments. Therefore, more people areencouraged to own individual insurance policies, or enlarge the insured amountsif they have already owned them.

In order to facilitate the development of the industry, and provision of'nore professional services and catering to clients' needs, a new profession calledinancial planning has been introduced. Finally, because comprehensive lawsind regulations must exist in order to monitor the industry development, therole of the Monetary Authority of Macau and the procedures of enhancing qualityassurance have been covered. In particular, AMCM is responsible for enactingthe laws as well as overseeing the overall operation of the industry.

In sum, a better economy where residents have more disposable income tobe invested will help boost up the number of new insurance policies andpremiums. In turn, whenever the insurance industry expands and thus contributesto economy, the economy will also be growing. Such an interactive relationshipis especially true for economies that rely heavily on financial sectors.Furthermore, because the savings rate in Macau is very high, and the barrier ofentry to the industry is minimal, there is still a high potential of expansion eventhough many overseas insurance companies have opened their branches. Throughthis paper, it is hoped that a clearer picture of how the insurance industry inMacau can aid its residents with better financial planning for the future, andhence stimulate its economic growth, can be presented.

Notes

1 Ho, N.W. (2002). Financial Development and Economic Growth in Macau, AMCMQuarterly Bulletin, No. 3, April.

2 Please refer to Williams, Jr., C. Arthur, Michael L. Smith, and Peter C. Young (1998).Risk Management and Insurance, 8th edition, Irwin Mcgraw Hill.

3 See Ming Pao Daily, 20th August, 2002.

4 AMCM (2002a). Annual report 2001.

5 AMCM Decree Law No. 006/99/M.

6 AMCM (2002b). Macau Insurance Activity 1st Quarter 2002.

7 The expenditure-based gross domestic product is MOP49.8 billion in 2001 (AMCM,2002a).

8 Helpful comments from the interview with Miss Sally Long, who is currently a SeniorUnit Manager and Certified Trainer of major insurance company in Macau, are highlyappreciated.

9 Ming Pao Daily, 12th September, 2002.

10 It's market shares are 61.8% and 57.2% in 2000 and 2001 respectively.

11 The figure is extracted from the company's informational documents.

References:

1. AMCM (2001). Insurance System And Supervision.

2. AMCM (2002 a). Annual Report 2001.

3. AMCM (2002 b). Macau Insurance Activity 1st Quarter 2002.

4. AMCM (2002 c). Macau Insurance Activity Semi-Annual 2002.

5. Ho, N.W. (2002). Financial Development and Economic Growth in Macau,AMCM Quarterly Bulletin, No.3, April.

6. Williams, Jr., C. Arthur, Michael L. Smith, and Peter C. Young (1998). RiskManagement and Insurance, 8th edition, Irwin McGraw Hill.

* Assistant Professor in Finance,Faculty of Business Administration, University of Macau